There are many benefits that organizations can realize by leveraging a shared services delivery model for finance transaction processing, such as increased efficiencies, reduced costs, and increased productivity. For example, consider the following efficiency and cost metrics for the overall finance function from APQC’s last finance shared services data collection conducted in conjunction with management consultancy ScottMadden:

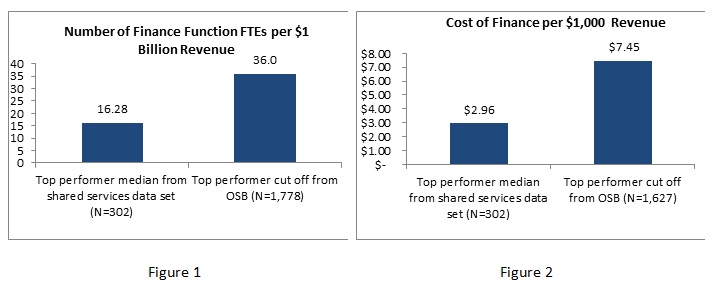

Figure 1 depicts the median number of finance function full-time equivalents (FTEs) per $1 billion of revenue, a finance efficiency KPI, and shows that the median of the top performers peer group from the shared services data set require only 16.28 FTEs per $1 billion of revenue (N=302) to perform all activities within the finance function. This compares to 36 FTEs per $1 billion revenue (N=1,778) for top performers (regardless of the finance service delivery model) from APQC’s Finance Organization Open Standards Benchmarking survey. Similarly, Figure 2 depicts the median total cost of finance per $1,000 revenue cost KPI, and shows that top performers in the shared services data set only incur $2.96 per $1,000 of revenue (N=302) for the finance function, which compares to $7.45 per $1,000 revenue for top performers (regardless of the finance service delivery model) from APQC’s Finance Organization Open Standards Benchmarking survey (N=1,627). So, in this instance, for both the efficiency and cost KPIs, finance shared services top performers have better results than those found in the larger data set.

While data such as this can provide a burning platform for change, your business case for transitioning to a finance shared service center will require additional due diligence, including working through the following questions:

- Business challenge(s): What specific business challenges or objectives will the new structure address, and how? How does the proposed finance shared services center support business strategy?

- Scope: What are the specifics of the proposed finance shared services initiative? What is included in its scope (which specific finance processes)? What is excluded? What specifically is it that you are proposing to do in terms of infrastructure, process, people, and/or content or technology?

- Market analysis: What is happening in the competitive and/or market environment, particularly the labor and regulatory environment, that is relevant to the proposed initiative? If you have conducted a SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis what has it revealed?

- Resourcing/Cost: What do you anticipate the new structure will cost in terms of start-up resources (fully-loaded labor, systems or technology, outsourcing cost, administrative or other costs, opportunity cost, etc.)? What do you estimate it will cost to maintain on an ongoing basis?

- Anticipated benefit: How much do you estimate that the new finance shared services center will save or benefit the organization in the short-term and in the long-term? Two popular financial metrics to estimate are return on investment (e.g., total estimated benefit of the investment divided by total estimated cost of the investment, expressed as a percentage) and payback period (e.g., how quickly you will recover your investment; the amount of the total initial investment, divided by estimated annual net cash inflow or savings, expressed in terms of number of years). Sometimes the anticipated benefit could be thought of in terms of cost avoidance; in other words, avoiding the cost or penalty of inaction.

- Staffing and Governance: What is the anticipated staffing model for the finance shared service center? What governance structure will the center employ? Will there be designated global process owners? Consider drafting a RACI (Responsible, Accountable, Consulted, and Informed) chart at this point.

- Risk analysis: What are the possible risks of moving to the proposed finance shared service center? What contingency plans will be made for overcoming these risks? What are the risks of inaction?

- Key enablers of/Barriers to success: What are the critical success factors for finance shared service center? What factors or barriers could keep it from succeeding?

- Proposed project measures: How will you measure the success of the shared service centers? You can use the APQC Open Standards Benchmarking data to conduct a baseline for finance current state. There may also be some “softer” or more qualitative success indicators that are relevant to this section.

- Timeline and next steps: While a detailed project plan is not necessary at this stage of the game, it is important to at least outline at a high level the timeline, key milestones, and specific next steps involved.

APQC’s benchmarks can provide a burning platform for change, a current state assessment, and performance targets to aspire to when it comes to finance shared services, along with the best practices for how to get there. And, for those who already have financial shared services up and running, consider joining us for our latest financial shared services data collection effort (currently underway), conducted with ScottMadden.